Taxable Investing Account vs. Roth IRA: Evaluating the Right Vehicle for Your Strategy [2026]

September 27, 2021

Thanks to Betterment for sponsoring this deep dive into the intricacies of the taxable Investing account vs. the Roth IRA.

Paid client. Views may not be representative. See App Store & Google Play reviews. Learn more. Investing involves risk. Performance not guaranteed.

Here’s the bottom line up front (BLUF?): If you (and your spouse, if applicable) wouldn’t be withdrawing more than the upper bound of the 0% capital gains tax rate in retirement, there may functionally be little difference between the Roth IRA and the taxable Investing account at the time of withdrawal.

(IRA contributions are limited to earned income and subject to contribution limits. Betterment does not provide tax advice.)

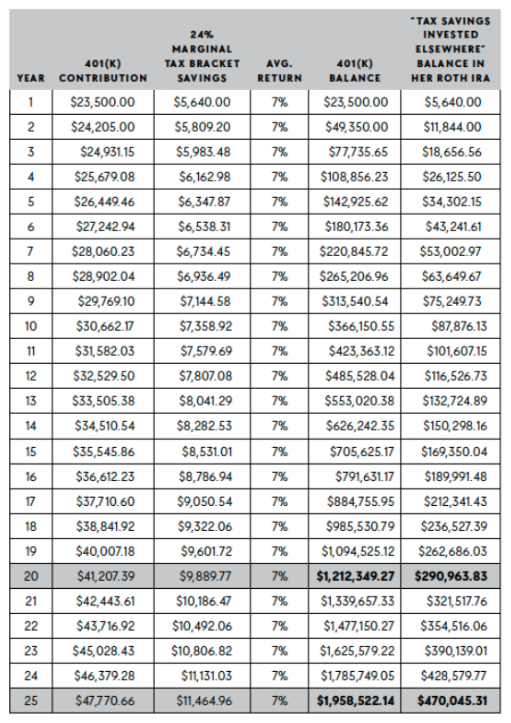

Merely typing that sentence felt blasphemous, but if you’ve read Chapter 6 of Rich Girl Nation, you know a critical part of my investment strategy involves being strategic about tax-advantaged investment vehicles such that you could reach your magic number approximately 13% faster.* (*Citation: Me and my special math, which is going to have to be a Just Trust Me Bro moment until you reach the appendix of this post, where I’ll include a picture of the graph.)

Because retirement (early or otherwise) in the United States is effectively the thing you invest to reach your entire working life and then use that money to pay yourself “a salary” later, navigating the taxes you pay on that income can make a meaningful difference in outcomes.

TL;DR: Withdrawals from your different accounts are taxed differently:

- Withdrawals from your pre-tax accounts like your Traditional 401(k) will be taxed as if it’s qualified income (though, no payroll taxes, so you’ll keep your 7.65%).

- Distributions from your Roth IRA and other Roth accounts may be tax free, if IRS requirements are met.

- And finally, gains realized in your taxable Investing accounts will be taxed in their own special tax bracket, the capital gains tax bracket, which reflects our country’s love affair with its capital class.

The entire premise privileges tax-advantaged accounts, which might make you think I’m less enthused about taxable Investing accounts. Not so. In fact, the strategy wouldn’t work without that long-term capital gains tax rate—because your capital gains can be taxed very favorably.

How favorably? Let me show you:

Up to $98,900 of qualified investment income can potentially be taxed at a 0% federal rate, a meaningful advantage when compared to ordinary earned wages, where an equivalent amount would subject a married couple to federal income and FICA taxes.

When you leverage the standard deduction ($16,100 for single filers and $32,200 for married couples filing jointly), the upper limit to qualify for the 0% long-term capital gains tax threshold expands even further. Taken together, individual scenarios may allow for the following thresholds:

- Single filers could realize up to $65,550 in income qualifying for the 0% capital gains rate when factoring in the standard deduction—the mathematical equivalent of a $5,462 monthly budget.

- Married couples filing jointly could realize up to a combined $131,100, which is enough to support monthly expenses of $10,925 under the 0% rate bracket.

If you can save and invest your way there in your pre-tax, Roth, and taxable accounts (this may be enough to generate tax-free income—if IRS conditions are met— of ~ $1.7 million for the single filer and ~$3.3 million for the married couple, using a 4% rule), you can generate tax-free income, provided there are no major changes to the tax code.

So you’re probably like, “Great, this isn’t news, Katie—we all read your dumb book and we’ve been over the fact that we can use our taxable Investing accounts to create $98,900 in tax-free capital gains income! What does the Roth IRA have to do with any of this?”

Instances where a taxable Investing account competes with a Roth IRA

One of the benefits of becoming financially independent is embracing flexibility and freeing yourself from a life that costs a lot of money. If you’re someone (or rather, a couple) who can live on $98,900 per year or less, I’d argue that the taxable Investing account makes almost as much sense as a Roth IRA in most circumstances, and more sense in others.

A key feature a Roth IRA offers is the potential for qualified, tax-free distributions if IRS requirements are met. If $98,900 in a given year isn’t enough (say you need to withdraw a much larger chunk to buy a home, or otherwise access a lot more of the money at once), Roth IRAs provide a highly compelling strategy from a tax perspective.

But here’s the headline: If you (and your spouse, if applicable) wouldn’t be withdrawing more than those amounts annually anyway, then the tax impact at the time of withdrawal can look remarkably similar between a Roth IRA and a taxable Investing account. Both can potentially carry the benefit of a 0% federal tax rate. The taxable Investing account simply has an upper limit for that specific bracket.

What about the tax-advantaged growth along the way in the Roth IRA?

As you likely know by now if you’ve been hanging around my corner of the internet long enough, a possible downside to a taxable Investing account is that you generally have to pay taxes on your dividend income every year, even if you choose to automatically reinvest it. If you’re just buying and holding index funds or index fund ETFs in your taxable Investing account and never selling (selling = realizing capital gains), you wouldn’t be taxed on your unrealized capital gains annually—but the dividends are a different story.

Let’s pretend your taxable Investing account contains one ETF: VTI, the Vanguard Total Stock Market ETF.

Assume that VTI has paid a dividend yield around 2% per year (give or take a few basis points).

If your taxable Investing account has, say, $1M in it, you’re going to get an approximate 2% dividend yield each year worth $20,000.

That’s a fantastic tiny violin problem to have (there’s really no world except for tax planning in which $20,000 of dividend income is considered “a problem”), but along the way, you’re going to be paying taxes on that dividend yield every year.

In that sense, it’s a race against the clock—you may want as few tax seasons as possible to pass between when you (a) start working toward your FI number in your taxable Investing account and (b) when your earned income drops and you begin living on that income. Once your earned income drops and you begin withdrawing your capital gains, your qualified dividend income could potentially become absorbed in that 0% bracket.

Assuming the dividends are qualified, they’d be subject to the same favorable capital gains tax rates as realized gains (0% up to $49,450 single/$98,900 married and 15% thereafter).

The amount of income tax you’ll pay on your dividends during your working life and accumulation phase depends on how much money you make, but most people end up paying 15% on them annually. This may not be a big deal when your account is small. For example, if a taxable Investing account with $50,000 worth of VTI earns an approximate 2% dividend, you’re paying 15% on $1,000 (about $150). But 15% of $20,000 (approximate 2% dividend yield on $1M) is $3,000.

That would mean—leading up to your drawdown of this account—your dividend yield would take a 15% haircut each year that you otherwise wouldn’t be subjected to within a Roth IRA, and that’s not nothing. If you increase the value of this account by $50,000 per year (starting with $100,000 and taking 19 years to reach $1M), you’d pay an estimated total of $31,350 in dividend taxes over 19 years assuming consistent tax rates and yields.

We can probably assume those tax payments represent opportunity cost. Even if we aren’t withdrawing the money from the account to pay the dividend tax, the income that we use to pay the taxes can no longer be invested. If you assume the average annualized dividend tax over that period ($1,650**) had been invested every year and gotten an average of 8% returns, we’d be looking at around $75,000 in opportunity cost.

**$31,350 over 19 years is an average of $1,650 per year, though in reality, your payments would start small and grow larger over time, not be perfectly uniform.

Over a normal working life of 30 or 40 years, the dividend taxes may add up. The earlier the “retirement,” the lower the opportunity cost of decades of dividend tax payments that a Roth IRA strategy is designed to help reduce.

The flexibility of the taxable Investing account is incredibly valuable

In order to produce income in early retirement, a taxable account can be an essential tool, because the contribution limits for the Roth IRA mean it can take a significantly longer time to accumulate enough to live on in an account with contribution limits.

And while some people have access to Mega Backdoor Roth IRAs (these enable you to contribute tens of thousands of after-tax dollars to your Roth IRA through some specific 401(k) footwork), I’m arguing that the qualified dividend tax burden could be a worthwhile trade-off if it means access to your money before 59.5.

Because while you can access your Roth contributions early, you can’t access the growth without potential penalties—and since your Roth dollars are tax-free, you may want to use them last to give them more time to grow. It’s safe to assume that money you put in your Roth IRA will truly be the last money you ever spend, if you ever get to it (some people find that their taxable accounts and 401(k)s grow large enough that they never even need their Roth IRAs).

The point is, overfunding the Roth IRA (especially in the “mega backdoor” situation) can result in underfunding the taxable Investing account, which, thanks to the long-term capital gains tax rate, can function with similar tax efficiency in retirement so long as your total income across all sources is lower than $65,550 (single) or $131,100 (married filing jointly).

You can think of the dividend tax like a fee for using your “no rules” investment account.

Interested in opening a taxable Investing account?

I recommend Betterment. Betterment offers taxable Investing accounts with a diverse mix of equity and bond ETFs, selected for you depending on your investing goal and the way you answer a few questions about your age and timeline.

Betterment’s automated investing accounts are about as flexible as it comes: There are no contribution or income limits, and Betterment can provide guidance to help you understand the tax impact of any withdrawals you make. The algorithm that constructs your index ETF portfolio is guided by the analysis of Betterment’s team of investing experts who work to help maximize potential returns, reduce your tax burden, and automatically rebalance and reinvest on your behalf.

Right now, when you open any individual investing account (including an IRA) with Betterment and make a deposit, and you can earn up to $2,000—on Betterment.

Appendix

As promised, here’s the “Invest in a Traditional 401(k), then invest the tax savings elsewhere” chart from Rich Girl Nation, which sadly will be fossilized with 2025 contribution limits and tax data:

The 7% return is a hypothetical assumption provided for illustrative purposes only and does not represent the performance of any specific investment. Actual returns will vary, and investments can lose value.