3 Ways to Lower Your Tax Bill in 2024 (and How to Navigate Those Weird Rollover IRA Forms)

As my standard legalese: I am not a licensed tax professional, and this is not tax advice. Please consult your friendly neighborhood CPA and do your due diligence. This is intended to be a starting point for your #TaxSzn research.

As I was reminded repeatedly by TurboTax’s 2023 ad campaign called “Don’t Do Your Taxes,” most people would rather scale an icy mountain than file their taxes.

While I absolutely used to feel that way, too, I’ve come to love tax season as a time for reflecting on my financial progress, collecting forms like rare Pokémon, and poking around my tax software of choice, TaxAct (not a sponsor, but you should be!), for deductions I didn’t realize I qualified for. (The part where the software tells me I owe tens of thousands of dollars is my least favorite part, but it’s decidedly fun up until that point!)

So, we’re discussing three ways to lower your tax bill that I’ll highlight below, but I also wanted to cover a few bizarre forms you may encounter when you begin dabbling in the world of deductible contributions to qualified retirement plans. (This won’t be exhaustive, but they’re items Henah or I have personally come across after implementing our own strategies.) It can be scary the first time you hit a speed bump in the tax software that’s like, “Yo, you may have screwed this up!”

Now, depending on how you earn and your access to retirement accounts and certain healthcare plans, it’s possible that all three of the options we cover today will be viable for you, but they all have one thing in common:

They’re all legal ways to hold on to more of your income, instead of forking it over.

Crucially, these vehicles allow contributions made this year—in 2024—to be characterized as though they were made last year, in 2023. And at the risk of stating the painfully obvious: To take advantage of this, you have to have the cash available to invest.

Which tax year should you select when making contributions in 2024 for 2023?

When you’re contributing to these investment accounts, they’re going to ask you which contribution year you’re electing. If you’re trying to ease your 2023 tax burden, be sure to select 2023! If you choose 2024, it’ll apply the contribution to next year’s tax bill.

The Traditional IRA and a few related fun formz

If you (and your spouse, if you have one) are not covered by employer-sponsored retirement plans at work (read: a 401(k) or 403(b), most likely), you can each contribute up to $6,500 to your own Traditional IRAs for the 2023 tax season.

That’s up to $13,000 you can wipe right off the top of your taxable income, if both partners contribute the full amount to their respective IRAs.

A minor point of clarification for couples with combined finances: These are intended to be individual retirement accounts, so there’s no such thing as a “joint” IRA.

How do I calculate the tax savings I’ll score from contributing to the Traditional IRA?

For example, if you and your spouse are in the 24% marginal tax bracket after other deductions and you both contribute the maximum allowed, that’s a joint tax savings of approximately $3,120 (a calculation we arrive at by multiplying our contribution, $13,000, by our marginal tax rate, 24%).

This means if you owed the IRS, say, $1,500, this one move would wipe out that tax liability, and probably generate a refund, too.

But here’s how your income may thwart your plan to deduct your contributions

Straight from the mouths of our boiz of the IRC, here are a few income limits and phaseout scenarios to be aware of for the 2023 tax season:

If you ARE covered by a workplace retirement plan…

A single taxpayer (or head of household) begins to phase out of being able to take a deduction for their contribution when their MAGI (Modified Adjusted Gross Income) exceeds $73,000, and is totally ineligible for a deduction once they earn more than $83,000

A married couple filing jointly begins to phase out of being able to deduct their contribution when their MAGI (We Three Kings, baby!) exceeds $116,000, and is totally ineligible for that sweet, sweet deduction once they earn more than $136,000

If you are NOT covered by a workplace retirement plan, but your spouse is…

A married couple filing jointly, where you are not covered by a workplace plan (but your spouse is!) begins to phase out at a MAGI of $218,000 and is totally ineligible once MAGI exceeds $228,000

And if you’re married filing separately, good luck—you can’t earn more than $10,000. (I know, I don’t get it, either.)

When this won’t work

To put a finer point on this one, this can only be leveraged to the hilt if you both aren’t covered by retirement plans at work.

Also note that you’re only allowed to contribute a maximum of $6,500 across your Traditional and Roth IRAs, so this won’t work if you’ve already contributed the maximum for 2023 (even if you were contributing to a Roth IRA, not a Traditional—but if you contributed, say, $3,000 to a Roth IRA, you’d have $3,500 left that’s fair game to contribute to either).

Fortunately, if you are covered by a plan at work and not eligible to consider a deductible Traditional IRA contribution, you can still contribute up to $6,500 to a Roth IRA (with some income limitations; here’s a video about how to get around those), though that won’t lower your taxes this year.

You can open a Traditional or Roth IRA at pretty much all major brokerage firms; I prefer roboadvisors for ease of use (think Betterment, M1 Finance, etc.), but if you choose to take the DIY route, remember to invest the cash you contribute. I know way too many smart people who opened an IRA, funded it, and never invested the cash, so it just sat there…for years…uninvested. We have an episode about indices to consider when you’re building a diversified portfolio.

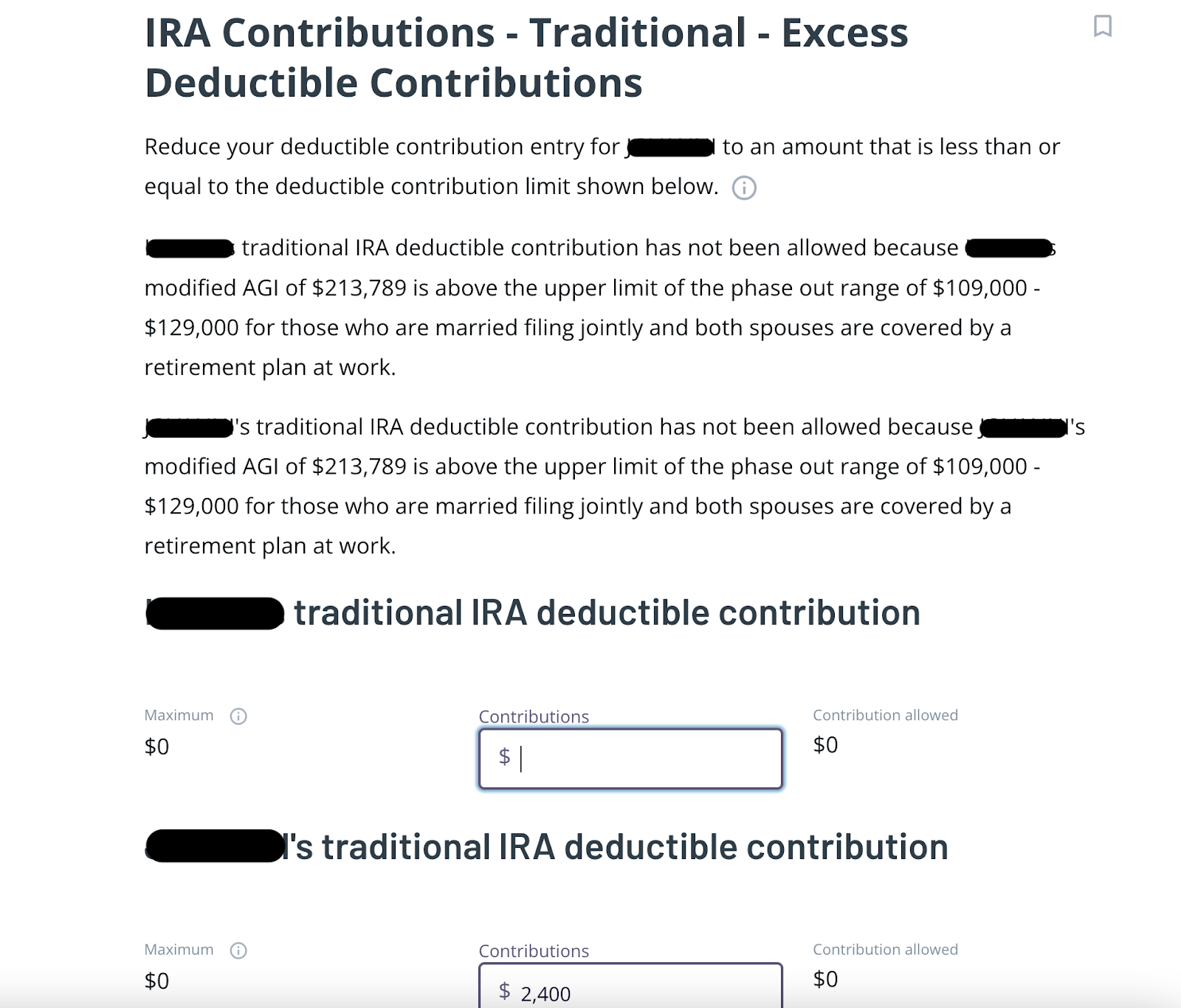

If you make excess deductible contributions, you’ll get prompted with a message (in TaxAct, at least!) that looks like this.

This screen grab is from the 2022 tax season.

Notice how TaxAct tells you what your maximum allowable deductible contribution is—in this case, the couple’s income, $213,789, was above the upper limit for a couple where both spouses are covered by plans at work in 2022.

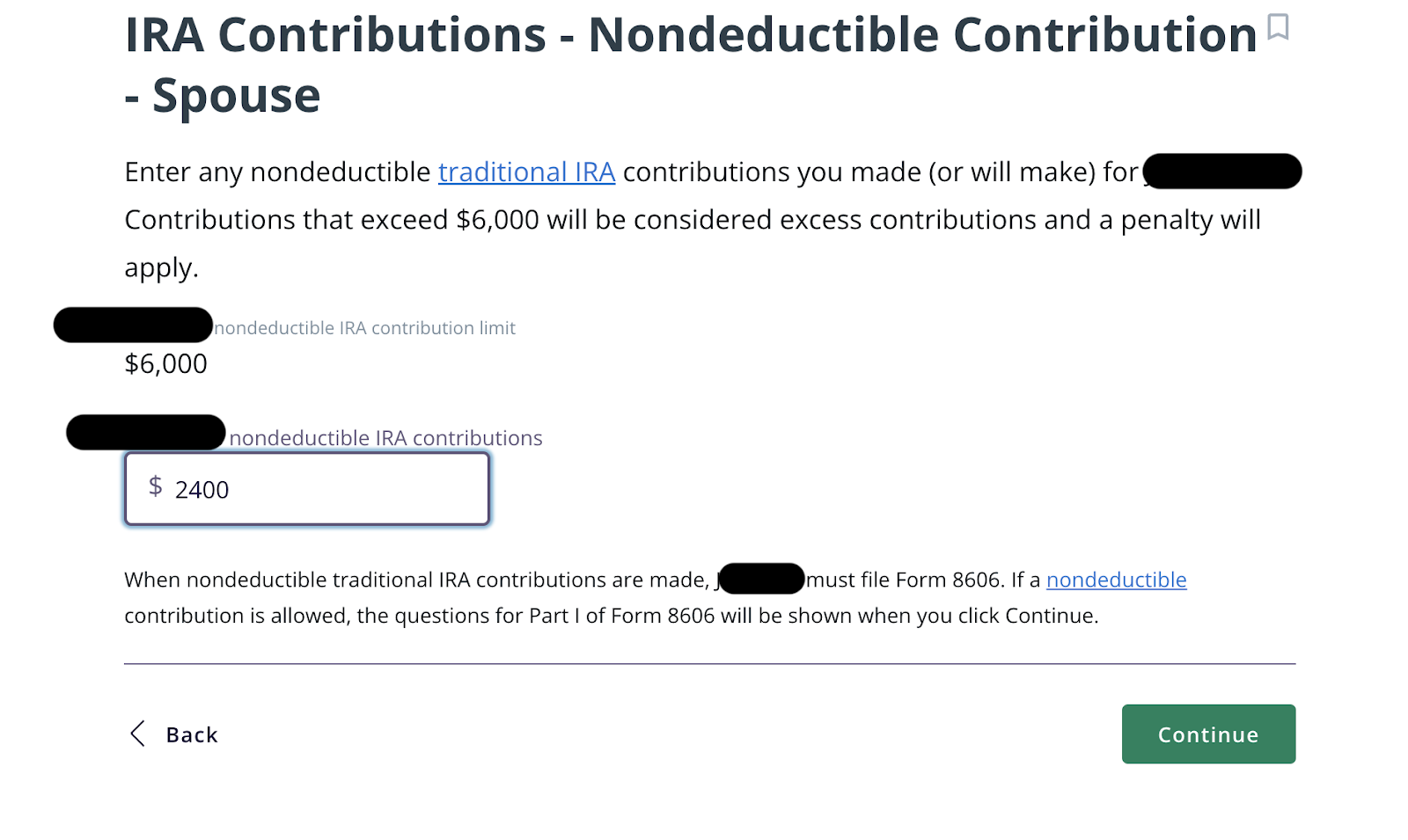

Form 8606 (I promise it’s not too scary)

All you need to do is file Form 8606, declaring that—oopsie daisy—you were totally just kidding, Uncle Sam, and your contributions were actually non-deductible all along!

That looks like this:

In this example, one individual in the couple accidentally contributed $2,400 to a Traditional IRA without realizing they couldn’t deduct the contributions. By classifying the entire amount as nondeductible, they’ve dodged the penalty bullet.

A quick jargon interlude: “Deduct” or “deductible” effectively translates to “wipe the amount off your taxable income as though it never happened.” Deductible contributions to pre-tax accounts are what allow us to save income tax in the present year. In this case, the couple became ineligible during the course of the year to deduct their Traditional IRA contributions, so the contributions become “non-deductible.” I.e., they’re no longer allowed to take the tax deduction.

So while you can easily fix excess deductible contributions by classifying them as “non-deductible,” you still won’t be able to deduct them (but they’re still tax-sheltered investments for the future, so all is not lost!).

And while we’re on the topic of Traditional IRAs, let’s talk about the 1099-R…

If you rolled over a 401(k) into an IRA in 2023, you received a form called the 1099-R. It’s a form your investment firm sends you whenever you take a distribution from a retirement account (yes, even a legal, unpenalized, run-of-the-mill rollover distribution!).

When I first received one a few years ago, I was convinced I was on a Pentagon watch list and had royally f***ed something up, but not to fear—this is a relatively straightforward declaration as well.

For example, in the TaxAct software, in the “Income” section, you’ll see an option for “Taxable IRA Distributions.” When you click on it, you’ll have the option to add a 1099-R. If you fill out the form exactly, it should include a few things:

The amount you rolled over

The “code” for the rollover

The taxable amount (if it was just a direct rollover that didn’t change tax status, it should say $0.00)

…and that’s about it. Regardless of your rollover amounts, filing your 1099-Rs shouldn’t impact your tax bill, but you’ll still want to make sure you report ’em. The IRS is ~super serious~ about transparency, you know?

Next up: The SEP IRA

If you have any self-employment income (read: 1099 income), this last-minute Hail Mary might be a godsend. Side hustle girlies, #rejoice.

A few things to note:

If you have a business with full-time employees, the rules are a little different; you have to contribute to their SEP IRAs, too, so if that’s your situation, you probably have a business CPA who can guide this choice—but if you’re just a solopreneur or side hustler, this is probably a fairly uncomplicated option for you.

You can contribute to a SEP IRA even if you’re also covered by, say, a 401(k) at a W-2 employer, since they’re accounts funded by two different sources of income.

The TL;DR on the SEP IRA for solopreneurs is that you can contribute up to 20% of your net business income, up to a whopping $66,000 for 2023.

If you want to calculate a super precise contribution for the biggest deduction possible, you can always pay a CPA to do it for you—but a tax pro I befriended (yep, I love me some tax nerds) taught me a cool trick to make this a little easier.

Since you deduct your self-employment taxes of 15.3% in order to get your “true” net business income on which the contribution is based, you can simply multiply your “self-employment income after write-offs” by 20%, rather than 25% (which is what you’ll see elsewhere online as the upper limit). This will give you a rough estimate of how much you can contribute to your SEP IRA.

So if your business earned $15,000 and you’re writing off $3,000 for expenses, leaving you with $12,000 of net business income before other deductions, you’d multiply $12,000 by 20%: You can contribute around $2,400 to your SEP IRA.

For those with a lot of side hustle or self-employment income, this deduction can be quite significant.

When this won’t work

This won’t work if (a) none of your income came from self-employment or side hustle-type sources or (b) you’ve already contributed the maximum to a Solo/Individual 401(k). For the uninitiated, a Solo 401(k) is just a 401(k) you can open for yourself and use as a self-employed person.

SEP IRA vs. Solo 401(k)

For example, if I had a Solo 401(k) in 2023 and I already contributed 20% of my net business income to it as “employer contributions,” I can’t then double-dip and contribute 20% more to a SEP IRA, too.

If you had a Solo 401(k) but didn’t fund it, you could finish funding the Solo 401(k) (with “employer” contributions) in 2024 for the 2023 tax year. That’s totally fair game, too—no SEP IRA required.

The reason the SEP IRA is a more viable option for retroactive tax minimization? You can’t open a Solo 401(k) in 2024 and fund it for 2023. The Solo 401(k) has to be opened by Dec. 31, 2023 to be eligible for 2023 contributions. That’s why the SEP IRA is such a baller tool—you could have started a business in 2023, made absolutely no moves to invest in pre-tax self-employment vehicles, and decide on April 13, 2024 that you want to open and fund one for 2023.

You can generally open SEP IRAs at all major brokerage firms without much fuss; roboadvisors typically offer them as well.

Beware of a SEP IRA if you do the Backdoor Roth IRA (and one way around it)

One watchout: If you’re currently someone who dabbles in the Backdoor Roth IRA strategy because you’re over the Roth IRA income limit, you’ll want to weigh your priorities before opening a SEP IRA, as a SEP IRA “counts” as a Traditional, pre-tax IRA and will make executing a Backdoor Roth IRA more complicated.

Sometimes, people opt for Solo 401(k)s instead for this reason. But if you’re down for a complicated workaround, you can open both a SEP IRA and a Solo 401(k) in 2024, fund the SEP IRA for 2023, and then—after you’ve filed and tax season is over—roll that shit over into your Solo 401(k) such that you have $0 balance in the SEP IRA again. Problem solved. Backdoor Roth IRA commence! Just note your business needs to be incorporated with an EIN number to open a Solo 401(k).

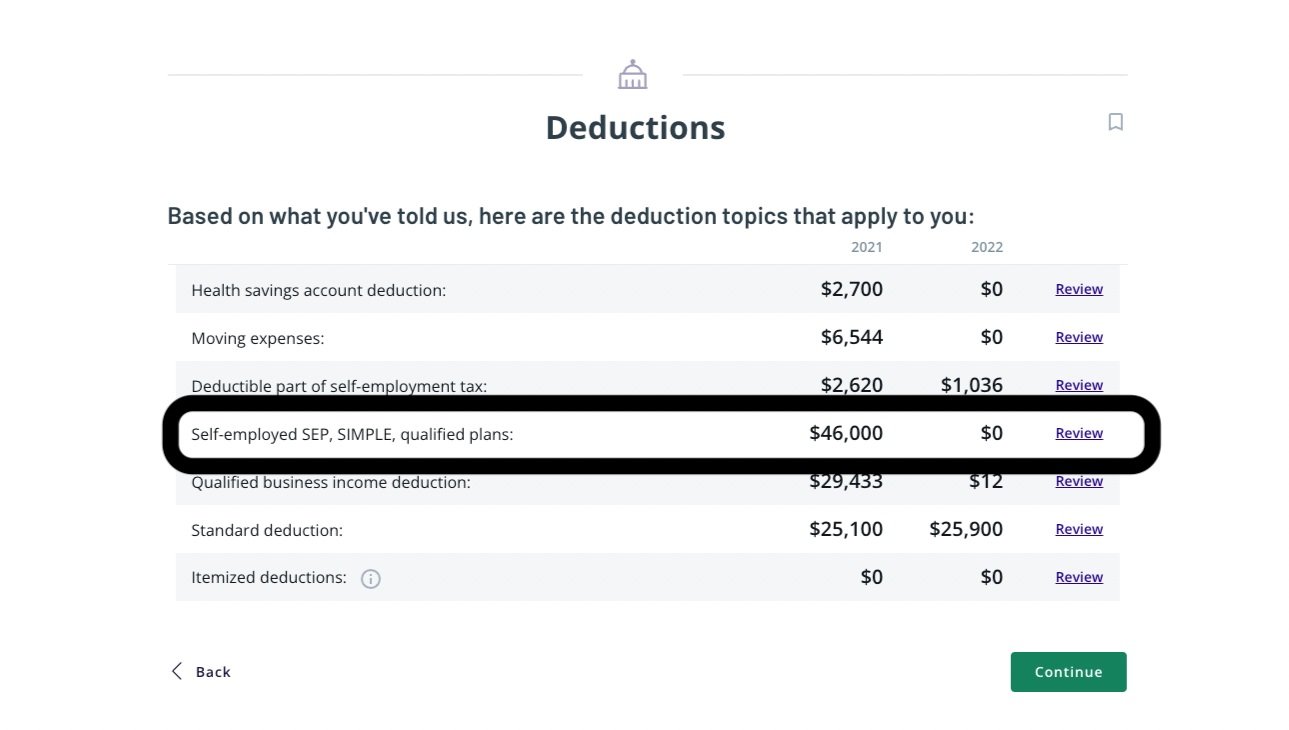

How to ~declare~ these glorious deductible contributions

Under “Deductions,” you’ll see a line item for “Self-employed SEP, SIMPLE, qualified plans.” That’s where you’ll tell the software how much you contributed, and “ooh” and “aah” as your tax bill lowers accordingly. As you can see, in 2021, my SEP IRA/Solo 401(k) contributions saved me an absolute boatload (yacht-load? We are talking about a billionaire’s game, after all).

And finally, the HSA—the consolation prize for our late capitalist healthcare hellscape!

If you have a high-deductible health plan (as defined by the IRS), you may be eligible for an HSA plan. The contributions and growth will be tax-free forever if you use the money for qualified medical expenses, so it’s a great place to rack up hella capital gains.

For 2023, the minimum annual deductible to be considered a high-deductible plan for self-coverage only is $1,500, and for family coverage is $3,000. The contribution limits vary on HSA plans for the 2023 tax year: If your health insurance plan just covers you, the limit is $3,850, and if your plan covers your family, it’s $7,750 for 2023.

You may already have an HSA set up through your work, or you may need to open one yourself, but once you surpass a certain amount of cash in the account (typically somewhere in the $1,000 to $2,000 range, but it varies by plan), you’re usually able to invest the funds—something you’ll do within your HSA account portal.

You’ll have to go to your HSA provider and make a direct contribution (as opposed to a payroll contribution) to contribute one big, fat lump sum, which is technically suboptimal because direct contributions aren’t exempt from FICA tax the same way payroll contributions are. The good news is, an HSA contribution made in 2024 can be retroactively tax-deductible for 2023.

Moving forward, consider making your 2024 contributions through payroll deductions, because then your contributions won’t be subjected to FICA tax, either! Woohoo! Another 7.65% saved.

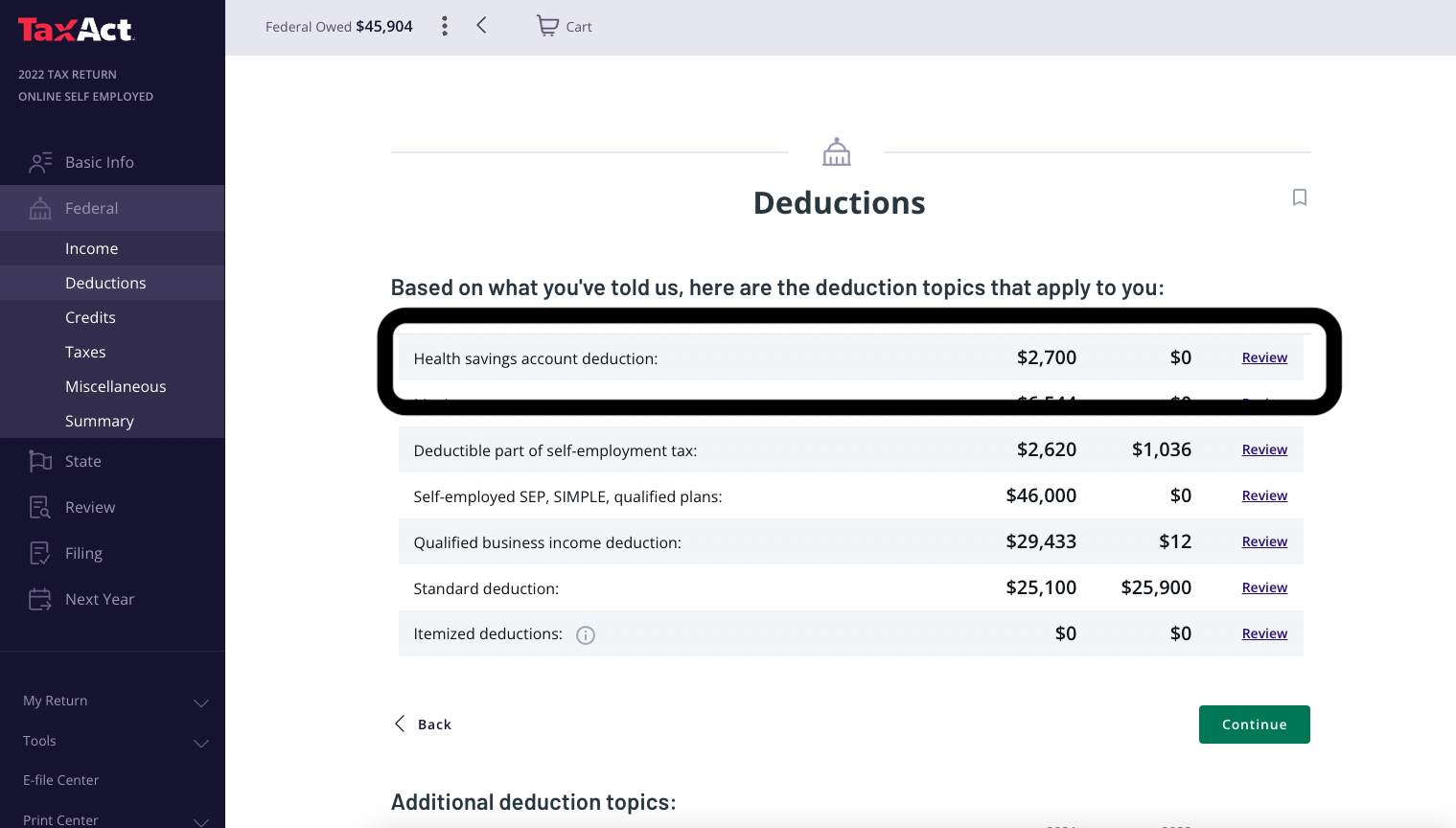

Any after-market HSA contributions (read: not payroll deductions, but new manual contributions) you make in 2024 for 2023 will be captured in the “Deductions” section:

When this won’t work

If you’ve already contributed the maximum to your HSA in 2023, unfortunately, this retroactive move isn’t an option (those contributions will be noted on the W-2 that your employer sends you). This also won’t work if you have a low-deductible plan.

The HSA is one of the best tax vehicles out there, because it’s effectively a second Traditional IRA that’ll never be subjected to required minimum distributions.

If you hang onto your HSA until you’re 65, it’ll basically “convert” to follow the same rules as a Traditional IRA, and you’ll be able to make withdrawals for whatever you want (not just health expenses) without paying a penalty. You’ll pay taxes on your withdrawals like you would with a Traditional IRA if you don’t spend them on health-related expenses, but that’s about it.

Someone who’s not covered by a retirement plan at work, has side hustle income, and has a high-deductible health plan could theoretically use all three methods.

Talk about a triple tax whammy! (I hate myself.)

It’s worth restating: I’m not a licensed tax professional. Please consult your CPA and do your own research before making big money moves. Hopefully this serves as a starting point for your pre-tax investing game this tax season if you haven’t made any decisions yet!