As a personal finance obsessor and generally well-meaning person, I find myself saying variations of this sentence a lot:

You NEED to start investing. It’s the EASIEST way to build wealth passively. Do you have time to look at quick compound interest chart? Are you interested in hearing the Good Word from our Lord & Savior, Jack Bogle, founder of the index fund?

And you know what? Most of the time, that’s true. In fact, when you zoom way out (I’m talking 50 or 100 years out) on a “stock market returns” chart, it feels inevitable. The line is choppy, but it’s mostly up and to the right.

Since I’ve started investing a few years ago, there have only been two big memorable “drops.” One was a blip, and the other was a crash-ier blip, but I’d still consider both blips:December 24, 2018 andMarch 16, 2020. Granted, March 2020 made December 2018 look like a bunny slope as it lost nearly 13% in a single day, but then something unforeseen happened:

This.

After the drop, the relentless climb upward continued, mostly unperturbed.

By August, it was back to its previous high, and now, a year later, it’s higher than it’s ever been.

Except, look around you: We’ve just sent out the third stimulus check. Unemployment is still high. Vaccine rollout is choppy. I don’t know that anyone would look at our economy and say, “Yep, that’s what you’d expect would be behind stock market all-time highs!”

How investing in the last decade has differed from investing in the past

In short, in the past 10 years, the market’s average annual return is around 14%. That’s… unbelievable. That means if you put $1,000 into VTSAX (the Vanguard Total Stock Market fund) in 2011, your total increase would be 274%, and you would’ve effortlessly turned $1,000 into $3,749.

Those of us who started investing in the last decade or so have been utterly spoiled with seemingly incredible returns, and while I’m happy our portfolios are doing so well, I worry that we won’t be mentally prepared for the inevitable losses that’ll likely follow over the next few decades. Not every 10-year period will feel like 2011-2021.

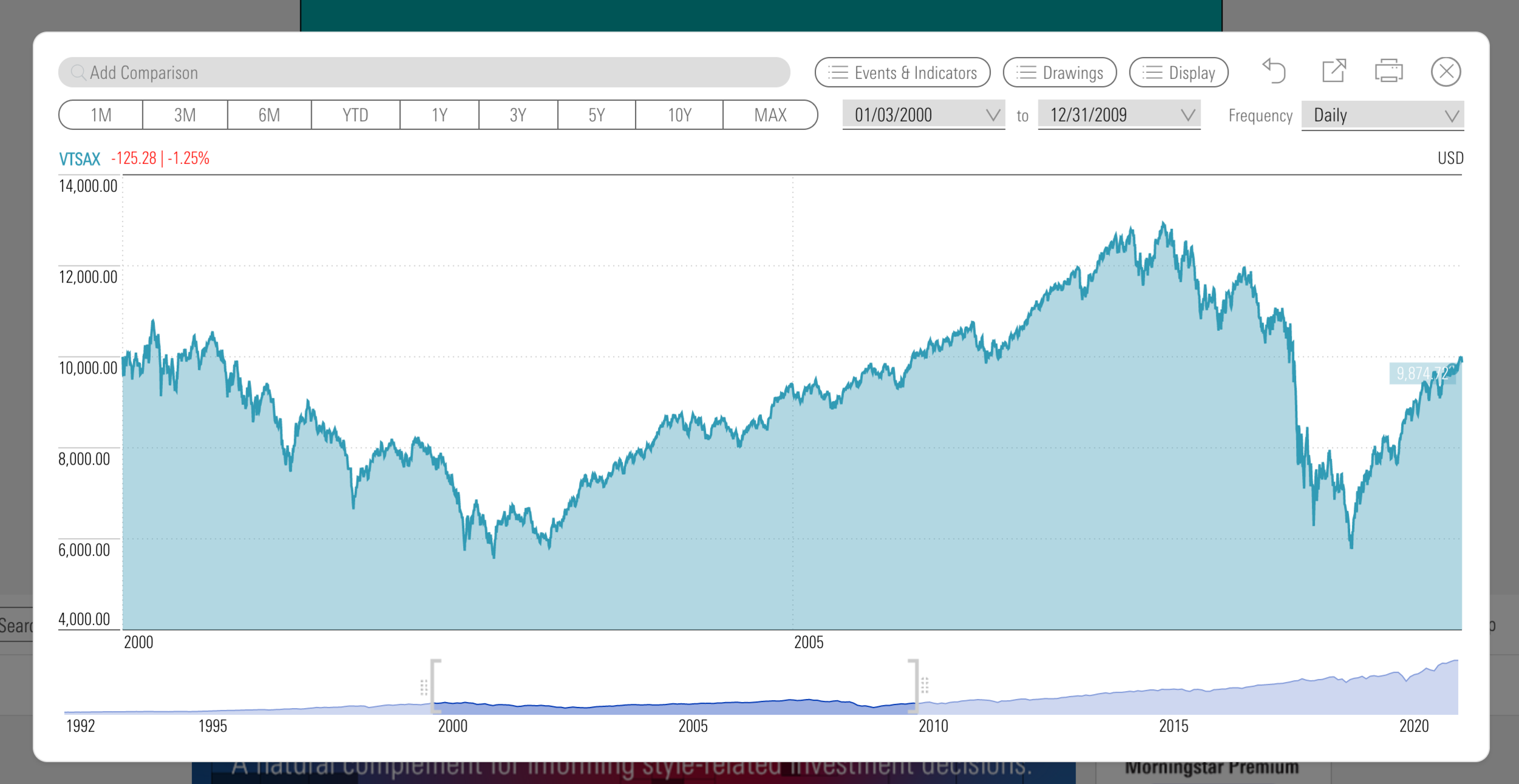

For example, let’s look back just one decade sooner:

If you had put $1,000 into VTSAX in December of 2000 and checked back in June of 2009, you’d have… less than $1,000.

I have to be honest, when I saw that for the first time, I thought, “Shit.”

That’s pretty demoralizing, no? Can you imagine investing your money in the so-called safest index fund in the game and ending up almost exactly where you started 10 full years later?

Now, obviously, the subtext is that this investor (hopefully) would’ve had the #guts to stay invested and trust that better things were coming: Had they stayed the course, today, they’d have $4,828 to show for their initial $1,000.

But the ride they went on from 2000 to 2010? They ended mostly where they started. It looked like this:

See the bracketed lines underneath the big chart that encapsulates that more or less flat period? Ugh. What a drag.

So yes, while I believe the stock market IS a relentless wealth-building machine, there will be times where you’re down: And sometimes it’s not just “down” in the same way that we were down in March; it’s not always a trampoline that propels us immediately back upward.

The point is, it’s going to test your nerves, and you have to have a long-term outlook to be successful – “long” meaning decades, not months.

How you can protect yourself from a lost decade

Well, the go-to answer here is diversification. Paul Merriman, one of my favorite financial educators, is a big fan of small-cap value funds.

(If you’re scratching your head like, Sis, WHAT?, let’s pause and talk about what the word “cap” means.)

You’ll probably hear large-cap, mid-cap, and small-cap most frequently when talking about index funds: and it stands for market capitalization.

This is a fancy phrase that essentially describes how big a company is.

When you think “small-cap,” don’t think the bakery down the street from you – “small business” on Wall Street ain’t the same thing as a small biz in your hometown: It means their market capitalization (what they’re “worth”) is between $300M and $2B.

On the contrary, a “large-cap” company is worth between $10B and $200B. That’s billion, with a B.

Paul Merriman loves small-cap value funds because historically they’ve outperformed the big boys. His explanation for this is rather compelling: Apple didn’t start out as Apple. It had to grow to get to the point it is now. When you own small-cap value funds, you own stocks when they’re considered a bargain – before they blow up. Most of them will fail and fall off entirely, but one shooting star that captures explosive growth can (and will) carry the entire index.

Rather than trying to seek out those tiny, fledgling winners and risk it all, owning a small-cap value index fund allows you to track the entire index.

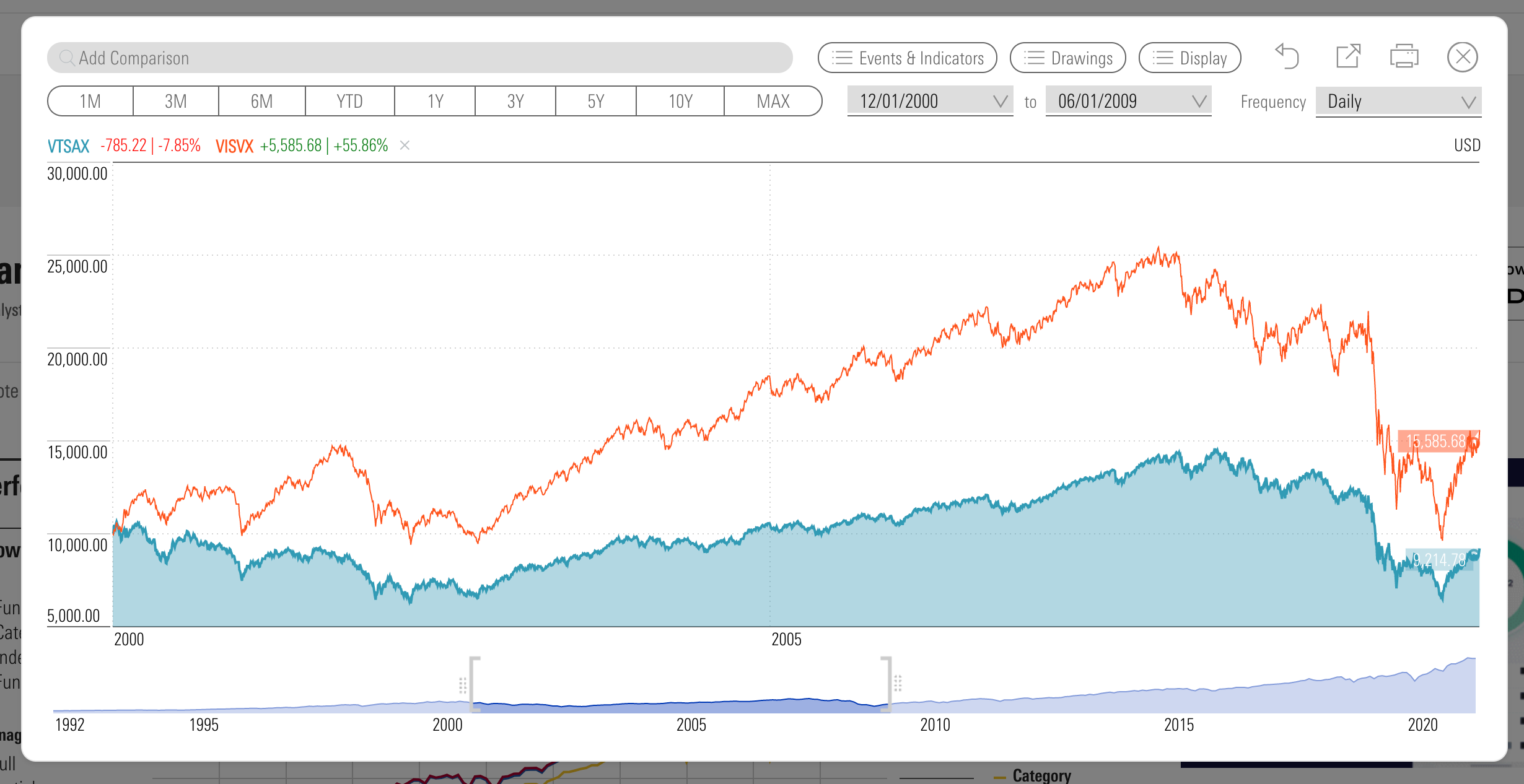

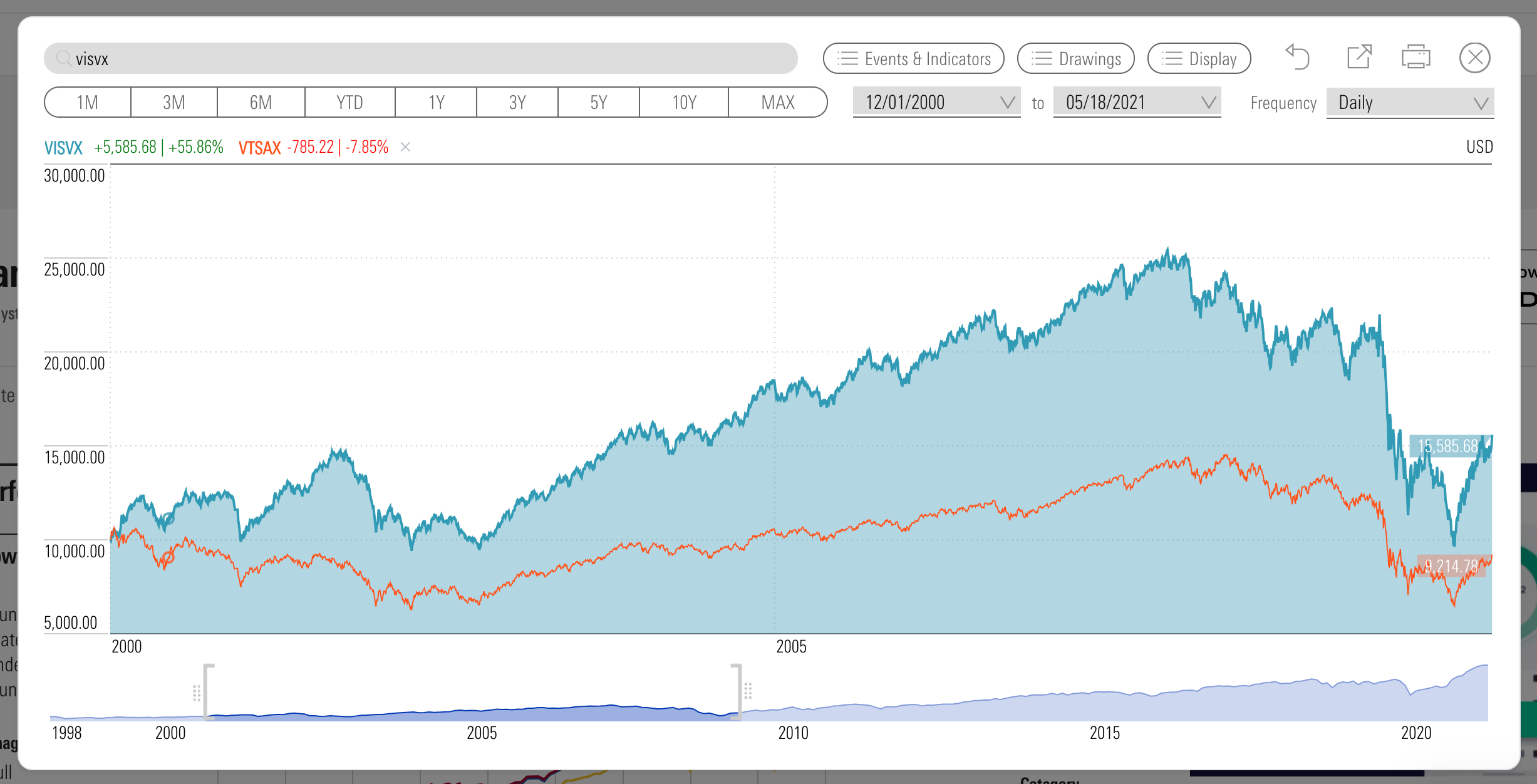

If you had been diversified during that time period from 2000 to 2009 we looked at earlier and owned some small-cap value, your returns would’ve looked quite different.

The blue line is VTSAX, and the red line is VISVX, the Vanguard Small Cap index. To be clear, that’s still a wild f***ing ride – but at least you would’ve come out ahead.

Those crazy ups and downs you see above are known as volatility. It’s an emotional rollercoaster, like dating a guy whose previous six girlfriends had the suffix “-eigh” on their names instead of an “-ey.”

So if you’re like, Well screw VTSAX, then, I’m all in on whatever the f*** she’s talking about now! Paul Merriman, where you at?

Not so fast.

Remember how we looked at our friend who put $1,000 in VTSAX in December of 2000 and would’ve been bummed in June of 2009 when their money was more or less where they started?

The past decade has not been kind to small-cap value, and large-cap funds have become the darlings of the day. Remember, historically speaking (looking back many decades, not just one), small-cap value has done better – and Paul Merriman would have me remind you, much better. But we investors are greedy, and we forget to look back at historical trends. We see performance since 2015 and think, Good enough for me.

Just take a look at the volatility of small cap value (the blue chunk) compared to large cap growth (the red):

This is why diversification matters.

But Katie, I thought you said VTSAX meant I was buying the entire stock market?

Well, it does! But it’s cap-weighted, which means bigger companies are given preference. For example, 10 stocks (out of 3,500+) make up more than 20% of the total value of VTSAX. Amongst them? Apple, Tesla, Facebook, Google, Microsoft. You know, the darlings.

You have a lot of large-cap exposure if you’re in VTSAX, and only a little small-cap (less than 10%).

This isn’t meant to scare you or over-complicate your strategy

After all, if you’re investing with a roboadvisor, you own a lot more than just a total stock market fund – you’ve got small-cap, mid-cap, emerging markets, international funds, and more (you can click into your “Holdings” tab to see what, exactly, you own).

JL Collins (the author of The Simple Path to Wealth) would say that’s all unnecessary and you’ll be fine if you just hold VTSAX (and if 2000-2021 is any indication overall, he’s right), but the point is this:

Those of us that have started investing since 2011 have been blessed with a decade of mostly Gatsby-tier returns and very little hardship

The hardship will come. It always does. It’s not a matter of if, but when and how hard.

And if your portfolio loses half its value overnight, it’s important to steel yourself to the fact that it may be more than just a couple “down” years – you may be looking at a bleak decade. But if you diversify (either with a robo, or on your own) and practice sincere commitment to a long-term mindset, you’ll weather the storm.

Paul Merriman wrote a book I read recently called We’re Talking Millions, and I’d recommend it if this small-cap value stuff interests you.

Remember that we’ve been blessed with great returns. Enjoy them while they come.

In conclusion

At the end of the day, it’s easy to look back at a decade where we’re averaging 14% per year and say, “Investing is easy. Growing my wealth is easy. I’m practically printing money over here.”

A monkey with a Robinhood account could’ve made money over the last decade.

But when you look at it over the longer term (50 years; 100 years) what you begin to see is that really, you shouldn’t hope for much more than 6-7%. Hope for the best, expect the worst.

This is why I get frustrated that we’re all jinxing ourselves in ~ personal finance Instagram world ~ where people post graphics with an expected return of 10%. 10%! Obviously our money is going to explode if we average 10% per year in perpetuity! But it’s just not likely.

I try to weigh my options realistically. I know I could lose half my portfolio in a down 5-year period. I know it may not recover for another 5 years. I know I’m taking a risk when I invest, and that past performance really isn’t indicative of future returns. That’s why I spend a lot of time emphasizing increasing your save rate (so your life requires you spending less) and minimizing your tax liability (because that’s another thing we can control).

What the market does with our contributions is a crapshoot. We can look back and pray things will continue the way they have been, but what I always fall back on is this: My alternative is a high-yield savings account that’ll definitely earn less than 1% per year (right now). To me, that’s riskier than betting on the stock market, because that definitely doesn’t beat inflation. Statistically speaking, if I’m diversified well, I know I have a decent shot at at least outpacing inflation and maybe doing a whole hell of a lot better.