Accidentally Contributed to a Roth IRA? Don’t Make My Mistake: A Case Study of Errors [2025]

January 31, 2022

The original tiny violin problem: Wah, I made too much money to contribute to a Roth IRA, and accidentally contributed to one anyway!

In other words, my life this year.

This is a weird transition that most people who (a) are actively earning more money and (b) contributing to a Roth IRA will probably experience, especially if your income is at all variable.

Who can’t contribute to a Roth IRA?

Single people making a MAGI (modified adjusted gross income) of more than $165,000 and married people making a MAGI of more than $246,000 in 2025.

The first time I saw the acronym MAGI, my brain short-circuited. I thought, “Cool, I’m nowhere close to that, I’m good to go!” But in the back of my mind, I wondered how people whose income was structured differently (or were on the edge) should think about it. For example, what if you made $160,000 base and had the potential to make a bonus of up to $10,000 per year? Then what? You might be completely unable to contribute, but how are you supposed to know until it’s the end of the year?

Those were what I considered to be silly rich people problems, so I didn’t lose too much sleep over it – but for practical purposes, if you fear you’re on the edge, here’s how I think about it:

MAGI, as we’ve noted, means modified adjusted gross income. For most, what this will mean in practice is that you want to remember your deductions. Your average person making somewhere in the ballpark of the income limit is likely contributing the maximum to a Traditional 401(k) which means – in 2025 – you can actually make quite a bit more than $165,000 or $246,000 and still not be completely precluded from contributing.

In our previous example, let’s pretend our friend who made $160,000 base also earned their full $10,000 bonus, for a gross income of $170,000 (this is assuming they didn’t have any interest, dividend, or capital gains income, but for the purposes of this example, I don’t think we need to go fully balls-deep into a complicated tax scenario).

$170,000 is – obviously – more than the Roth IRA income limit, so this individual might think they’re hosed.

Not so, my friend!

Assuming this person is single and contributing $23,500 to their Traditional 401(k) in 2025, that knocks their MAGI down to $146,500, below the low end of the phaseout limits.

All that to say: Make sure you’re factoring in your deductions when calculating whether or not you’re above the Roth IRA contribution limit.

A bit of good news: You have until April 15 to figure it out

While 401(k) contribution periods run January 1 to December 31, Roth IRA contribution windows run until you file your taxes (which is April 15 this year).

This means that if you’re really not sure where you’re going to end up each year, you could theoretically wait until January to see your total taxable income for the year, calculate your MAGI, and then contribute (or backpedal) accordingly.

So you’re over the limit, and you’ve already contributed – now what?

If you’re cursing the Money with Katie name because my MAGI preamble didn’t apply to you, don’t worry – we’re still going to cover how to handle this issue, though the brokerage firm that you work with may handle things a little differently (regardless, though, the terminology and process should more or less be the same).

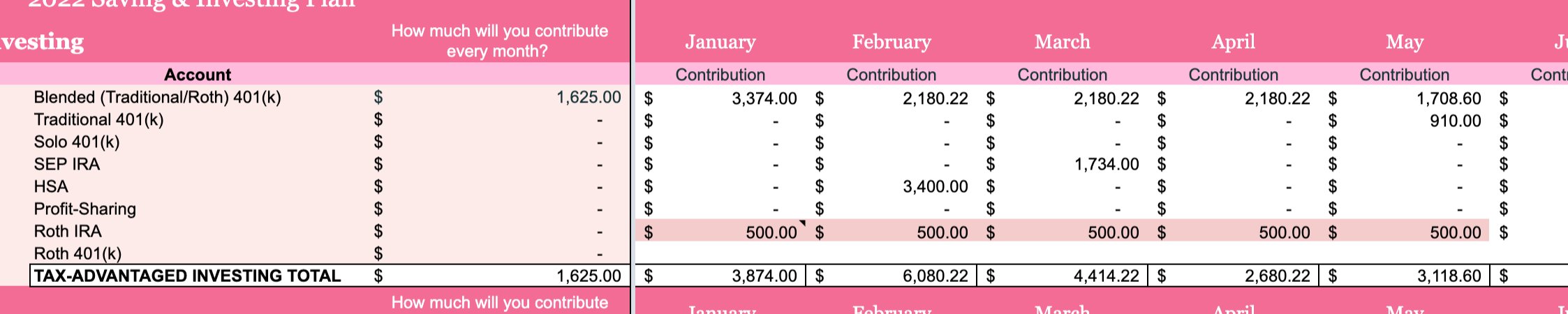

I opened a new Roth IRA in 2020-2021 with M1 Finance (because I wanted to test out their service after hearing about it on ChooseFI) and began funding it. Thanks to my handy dandy Wealth Planner, I know exactly how much I contributed and when. Observe:

Notice how I marked in red where I had contributed to a Roth IRA this year. (2021 Wealth Planner pictured.)

May 2021 was the, “Wait a second – I think I’m going to be too far over the income limit to deduct my way back down. Better stop adding fuel to this tax-free fire just in case,” moment.

That’s a good place to start. Figure out how much you’ve contributed in error. If you don’t have a Wealth Planner (shameless plug!), you can just look at the transaction history in your Roth IRA and filter by “deposits” or “contributions,” depending on your brokerage firm.

I added $2,500 to mine in 2021 and – in short – needed to remove those excess contributions.

Roth IRA contributions can be withdrawn at any time without penalty, but the earnings can’t be

Obviously, the entire point of funding a Roth IRA is to invest your money for tax-free growth. My $2,500 wasn’t sitting there uninvested with its thumb up its ass – it was earning.

So while I knew I could pull out my contributions without issue, I was confused about the earnings.

I submitted a Support ticket to M1 Finance and got this message back from a dude named Dexter. Let’s decode it below (my thoughts in italicized parentheticals):

Hi,

Thanks for reaching out to M1 Finance. (You’re welcome, Dexter.)

Unfortunately, it is past the deadline for our firm to change the contribution year for one of your deposits to a 2021 year instead of 2020. Only your excess contribution can be removed after this deadline.

(Shit. I was afraid of this. I had asked if we could potentially re-characterize my 2021 contributions that occurred before the filing deadline to 2020 contributions, when I wasn’t over the income limit, but no dice.)

To fix this, you can simply withdraw the over-contributed funds from your M1 account using the Transfers tab on the Web platform. Please select “Excess Contribution Removal, After Tax Deadline” as the reason. You will remove only the amount of the excess; no earnings or loss will be calculated.

(It took me a while to figure out how to do this, but basically, it was a designation during the withdrawal process where I had to select the bolded option. This part threw me for a loop, though, because I was withdrawing BEFORE the tax deadline – but I trusted Dexter without listening to my common sense.)

You will owe the IRS 6% excise tax for every year the excess remains in the IRA. Additionally, you may not deduct the excess amount when fling your taxes. The excess amount removed will not be taxable if your aggregate contributions for the year do not exceed the annual contribution limit.

(Pretty sure he included the language about not being able to deduct the excess amount to cover Traditional IRA scenarios, because Roth IRA contributions aren’t deductible.)

However, if your aggregate contribution limit for the year exceeded the annual amount, then the excess is taxable and would be subject to the IRS 10% additional tax if you are under age 59½. For example, you made a $6,000 Roth IRA contribution but only qualified to make a $5,000 contribution. The $1,000 excess would not be taxed and penalized because it wasn’t more than the annual contribution limit.

(All right, Dexter, you’re making my head hurt.)

Thanks,

Dexter

All right – got all that?

Didn’t think so.

I moseyed over to my Roth IRA in M1, found the Transfers tab, and withdrew $2,500 from my Roth IRA. I ain’t going to lie – it hurt me.

But I still wasn’t sure: What about the earnings? Wouldn’t the growth of that $2,500 get taxed or penalized in some way? Help me, Dexter.

I replied and asked what the deal is, and this is what I heard back:

Hi Katie,

Thanks for reaching out to us about your 2021 over contribution. Because the over contribution occurred in tax year 2021, we will need to re-code this withdrawal as a “before tax deadline” excess contribution removal. We will submit this change to our clearing firm to make the correction. As for gains, or Net Income Attributable (NIA) of the excess contribution, you’ll want to remove those funds by making an “excess contribution removal, before tax deadline” withdrawal as well, and indicate that the full amount withdrawn is the Net Income Attributable.

Please let us know if you have any questions, and we will provide an update once we have heard back from clearing firm.

Best,

Brokerage Operations

M1 Team

So what did we learn? Katie should always trust her gut, instead of Dexter (just kidding) – but it sounds like I was initially misdirected in choosing “After the Tax Deadline,” and I should’ve followed my gut there.

How to calculate (and withdraw) the earnings on your over-contribution

Regarding the gains in the account, they’re evidently called Net Income Attributable in the #biz, and while it’s good to know I have to withdraw those, too, I’m still left with questions:

-

How am I supposed to calculate the gains on my $2,500 contribution? I suppose I could go in and look at the growth this year, but that would show me overall growth of the entire account – not just this year’s contributions. I replied and asked if they could provide that number for me (and now I’m growing increasingly annoyed that this feels like a demented scavenger hunt).

-

Am I going to get taxed or penalized for the NIA withdrawal? I wish they had clarified what that MEANS!

Fortunately, they sent over a Support article that initially frustrated me but ended up being pretty helpful. And while it absolutely gave me PTSD to AP Physics WebAssign, I finally figured it out:

In order to calculate your NIA, you have to know:

-

Your excess contribution [how much you contributed that you shouldn’t have; in this case, it’s $2,500]

-

Your opening balance [what the account value was before you made the excess contributions; in this case, it’s $14,875.33, and I figured that out by looking at my 2020 end-of-year statement for the balance on Dec. 31, 2020, before I made any 2021 contributions]

-

Your closing balance [what the account value is now, after the contributions and their #gains have had a minute to marinate; in this case, it’s $20,007]

-

Your “adjusted” opening balance [which is just the opening balance plus the excess contribution; in this case, it’s $17,375]

Got all that? My Roth IRA was valued at $14,875 at the end of 2020, and throughout 2021 I made $2,500 of illicit contributions, which bumped it up to $17,375. Because of growth, it became worth $20,007.

Here’s the calculation to calculate excess growth

Take your old closing balance and subtract your adjusted opening balance: $20,007 – $17,375 = $2,632

Divide the answer, $2,632, by the adjusted opening balance: $2,632 / $17,375 = 0.15148

Multiply the answer, 0.15148, by your excess contribution, $2,500: $2,500 * 0.15148 = $378.70

This means my excess contributions of $2,500 were responsible for $378.70 of gains in 2021, so I need to remove them (and pay taxes on them).

How it’s coded matters

Remember how the Support peeps wanted to verify with me that the distribution was coded with their clearing house as an “excess contributions removal, before the tax deadline”? That’s because while I could’ve removed my initial $2,500 deposit without issue, ordinarily, I’d need to pay a penalty for withdrawing the earnings. The Roth IRA’s whole shtick is that it allows your contributions to grow tax-free, and we aren’t allowed to touch that sweet nectar until we’re 59.5 or older.

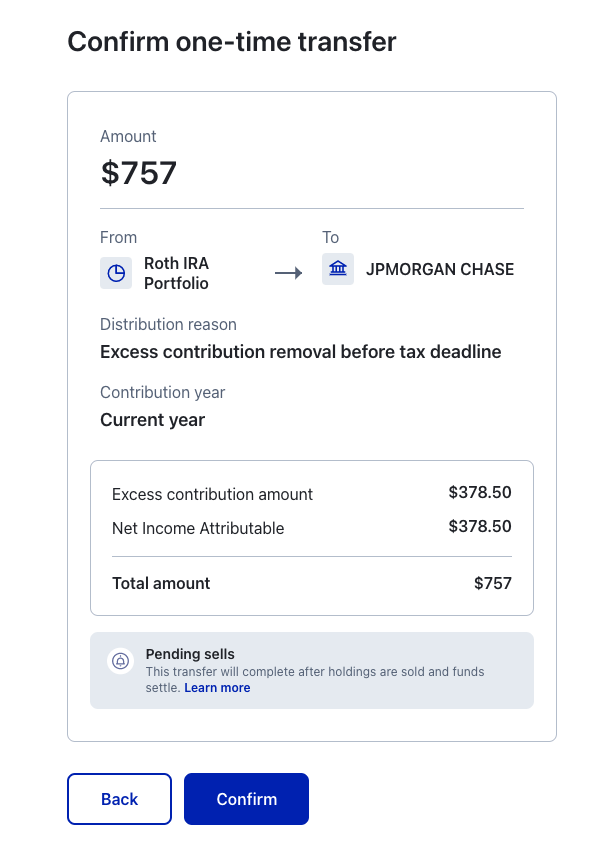

To round out this fiasco, I accidentally withdrew the $2,500 in one single transaction before I knew about NIA (because Dexter failed to mention it!), and when I went back into withdraw the NIA separately, it asked me for an NIA calculation. I input the same amount, but:

As you can see, M1 Finance thought I was trying to withdraw $378.50 as my excess contribution and another $378.50 as the NIA (earnings). If Dexter hadn’t steered me off a cliff, I would’ve known to calculate the NIA ahead of time and remove it with the $2,500.

Argh. Blocked again.

What to do if you remove the excess Roth IRA contribution without removing the NIA, or earnings

I circled back to my Support pals and asked how to handle this, screenshot in hand. They instructed me to withdraw $1 as my “Excess Contribution Amount,” then plug in the $378.50 as my “Net Income Attributable.” I did it, and the money was removed. It sounds like this is a tenable way to backpedal in case you’ve already withdrawn the excess contribution but forgot to pull the earnings.

What happens next: The 1099-R form

To close out this fiasco, you’ll receive a 1099-R form: the form that gets generated anytime you make a distribution from a retirement account. You’ll want to double-check that the word “Corrected” or “Corrective” is on the form to validate to the IRS that you weren’t just retrieving retirement funds for Coachella wristbands. You want the IRS to know you were legitimating your contributions for the year like the good little Rich Girl you are, right?

Is legitimating a word? I don’t know, but in this context, I think it works.